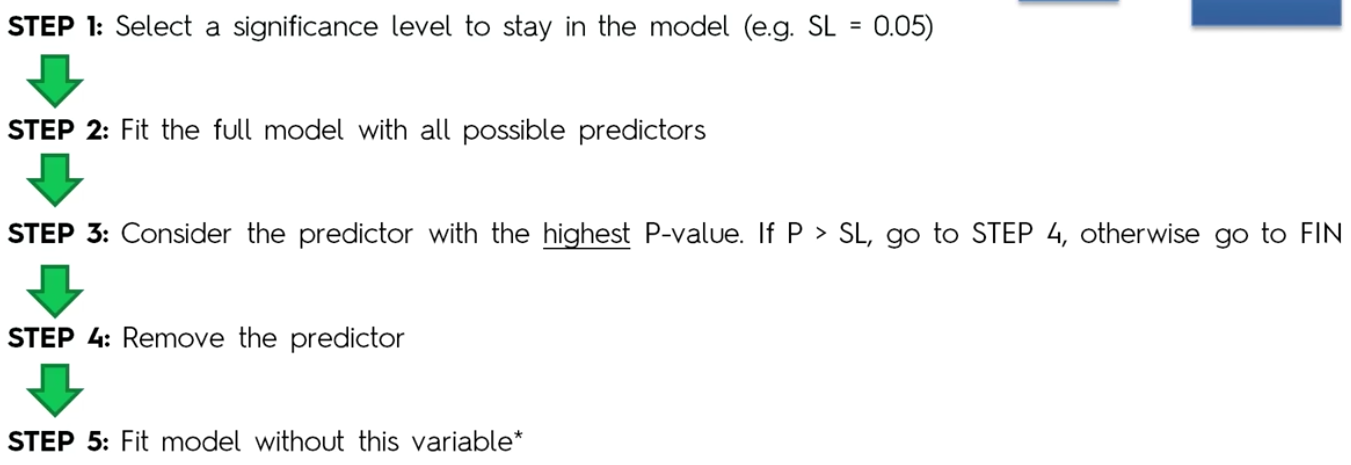

In the previous post, we learnt about multiple linear regression. The problem with the last approach was that we used all the features without considering that some of the features may not be impacting or playing any role in the outcome. we also talked about 5 ways of reducing the noisy feature. Backward elimination is one of them.

How to get the dataset?

What is Backward Elimination?

Backward elimination is a process to remove features that have little effect on the dependent variable.

What could possibly be wrong with leaving the features if they are not impacting or have little impact?

New England Patriots won the Superbowl on Feb 3, 2019. The team won because it had a better team, better skills and a good coach. If I say, the team also won because Patriots fans are great at cheering and that when Patriots play fans supporting the opposition is more tamed, then I would be wrong. If I say that all players in the team wore a white jersey and they won. They also won because they played it on Sunday and T. Brady thinks that it’s his luckiest day. You would call Baloney to all the facts that I just mentioned. It may have helped - may be slightly but too insignificant to make a real difference. The features in a data set are exactly that - Baloney. They only add noise in the actual model and many small non-significant data may actually provide us a model which is way off the margin. The simpler the model, the better the result.

How do we implement Backward elimination?

In backward elimination, you take all the variables and create the algorithm. Select a significance level, then consider the predictor with Highest P-value and if P-Value > Significance level then eliminate the variable from the equation, else keep it.

How do we implement it in python?

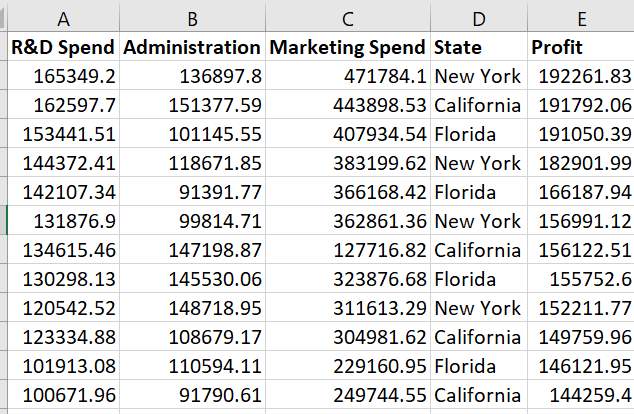

In the previous post, we were trying to figure out if a company is profitable or not by looking at 4 independent variables - R&D Spent, Administration cost, Market spending & State. We created a model with all the features. So let’s pick up from where we left off. Here’s how our dataset looks like

|

|

[-9.59284160e+02 6.99369053e+02 7.73467193e-01 3.28845975e-02

3.66100259e-02]

42554.16761772438

Train Score: 0.9501847627493607

Test Score: 0.9347068473282446

Take note of Train Score and Test Score

Train Score: 0.9501847627493607

Test Score: 0.9347068473282446

The difference between them is 0.01547791542 or 1.548%

So far we used all the features. Now to use backward elimination we will use an entirely new package and class. However, before we begin, we need to decide on a significance level. In this case, let’s chose a level equal o 0.05.

|

|

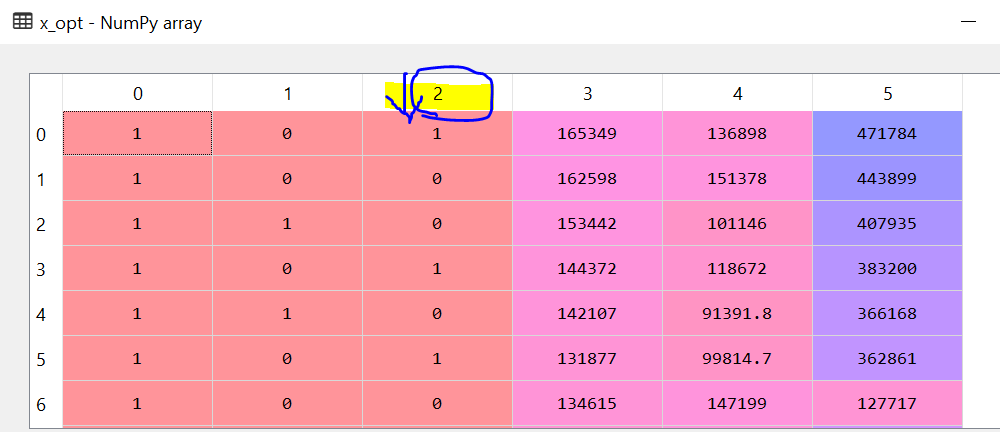

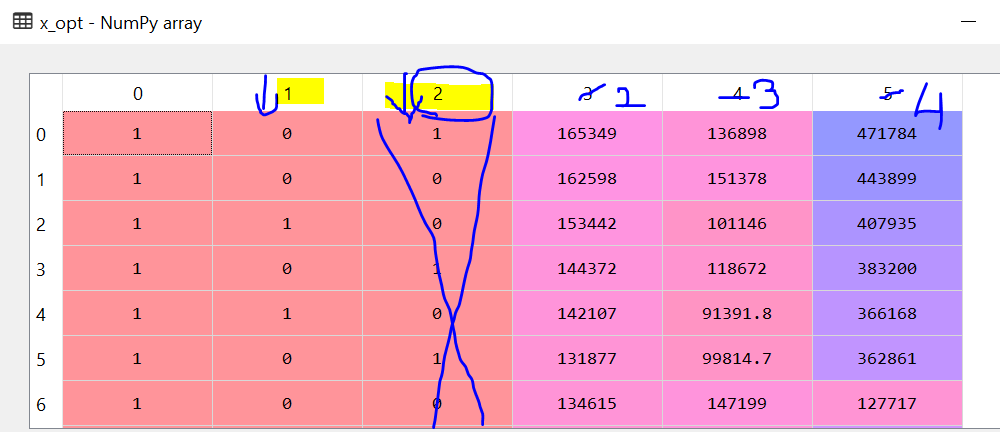

Why did we append 1’s in the existing dataset?

Y = b0X0 + b1X1+ b2X2 + b3X3 + b4X4 + b5X5 + C

In the above equation, if you notice that every Xn has a multiplier bn but not the constant C. Actually if you have a X6 and set it to 1 that solves the problem. The question is why do we need a 1 multiplier for the constant. The answer lies in the library and the class that we use. The package statsmodel only considers a multiplier if it has a feature value. If there is no feature value then it would not get picked up while creating the model. So the C would be dropped. Hence we need to create a feature with value = 1.

|

|

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.951

Model: OLS Adj. R-squared: 0.945

Method: Least Squares F-statistic: 169.9

Date: Sun, 10 Feb 2019 Prob (F-statistic): 1.34e-27

Time: 22:42:26 Log-Likelihood: -525.38

No. Observations: 50 AIC: 1063.

Df Residuals: 44 BIC: 1074.

Df Model: 5

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 5.013e+04 6884.820 7.281 0.000 3.62e+04 6.4e+04

x1 198.7888 3371.007 0.059 0.953 -6595.030 6992.607

x2 -41.8870 3256.039 -0.013 0.990 -6604.003 6520.229

x3 0.8060 0.046 17.369 0.000 0.712 0.900

x4 -0.0270 0.052 -0.517 0.608 -0.132 0.078

x5 0.0270 0.017 1.574 0.123 -0.008 0.062

==============================================================================

Omnibus: 14.782 Durbin-Watson: 1.283

Prob(Omnibus): 0.001 Jarque-Bera (JB): 21.266

Skew: -0.948 Prob(JB): 2.41e-05

Kurtosis: 5.572 Cond. No. 1.45e+06

==============================================================================

Based on the process, we now have to find the feature with the highest P-value and if it greater than ould SL then we will drop it. In this case

x2 has the highest P-value = 0.990 > 0.05.

So will drop the feature x2 which corresponds to the State dummy variable

We will continue and re-run the model with just 5 feature

|

|

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.951

Model: OLS Adj. R-squared: 0.946

Method: Least Squares F-statistic: 217.2

Date: Sun, 10 Feb 2019 Prob (F-statistic): 8.49e-29

Time: 22:52:32 Log-Likelihood: -525.38

No. Observations: 50 AIC: 1061.

Df Residuals: 45 BIC: 1070.

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 5.011e+04 6647.870 7.537 0.000 3.67e+04 6.35e+04

x1 220.1585 2900.536 0.076 0.940 -5621.821 6062.138

x2 0.8060 0.046 17.606 0.000 0.714 0.898

x3 -0.0270 0.052 -0.523 0.604 -0.131 0.077

x4 0.0270 0.017 1.592 0.118 -0.007 0.061

==============================================================================

Omnibus: 14.758 Durbin-Watson: 1.282

Prob(Omnibus): 0.001 Jarque-Bera (JB): 21.172

Skew: -0.948 Prob(JB): 2.53e-05

Kurtosis: 5.563 Cond. No. 1.40e+06

==============================================================================

Once again in the above output

x1 has the highest P-value = 0.940 > 0.05

So we will drop X1, which in this case represents the second dummy variable for the State.

So we will continue until we don’t have variable that is greater than our significance level

|

|

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.951

Model: OLS Adj. R-squared: 0.948

Method: Least Squares F-statistic: 296.0

Date: Sun, 10 Feb 2019 Prob (F-statistic): 4.53e-30

Time: 22:59:29 Log-Likelihood: -525.39

No. Observations: 50 AIC: 1059.

Df Residuals: 46 BIC: 1066.

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 5.012e+04 6572.353 7.626 0.000 3.69e+04 6.34e+04

x1 0.8057 0.045 17.846 0.000 0.715 0.897

x2 -0.0268 0.051 -0.526 0.602 -0.130 0.076

x3 0.0272 0.016 1.655 0.105 -0.006 0.060

==============================================================================

Omnibus: 14.838 Durbin-Watson: 1.282

Prob(Omnibus): 0.001 Jarque-Bera (JB): 21.442

Skew: -0.949 Prob(JB): 2.21e-05

Kurtosis: 5.586 Cond. No. 1.40e+06

==============================================================================

|

|

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.950

Model: OLS Adj. R-squared: 0.948

Method: Least Squares F-statistic: 450.8

Date: Sun, 10 Feb 2019 Prob (F-statistic): 2.16e-31

Time: 22:59:39 Log-Likelihood: -525.54

No. Observations: 50 AIC: 1057.

Df Residuals: 47 BIC: 1063.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 4.698e+04 2689.933 17.464 0.000 4.16e+04 5.24e+04

x1 0.7966 0.041 19.266 0.000 0.713 0.880

x2 0.0299 0.016 1.927 0.060 -0.001 0.061

==============================================================================

Omnibus: 14.677 Durbin-Watson: 1.257

Prob(Omnibus): 0.001 Jarque-Bera (JB): 21.161

Skew: -0.939 Prob(JB): 2.54e-05

Kurtosis: 5.575 Cond. No. 5.32e+05

==============================================================================

|

|

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.947

Model: OLS Adj. R-squared: 0.945

Method: Least Squares F-statistic: 849.8

Date: Sun, 10 Feb 2019 Prob (F-statistic): 3.50e-32

Time: 22:59:43 Log-Likelihood: -527.44

No. Observations: 50 AIC: 1059.

Df Residuals: 48 BIC: 1063.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 4.903e+04 2537.897 19.320 0.000 4.39e+04 5.41e+04

x1 0.8543 0.029 29.151 0.000 0.795 0.913

==============================================================================

Omnibus: 13.727 Durbin-Watson: 1.116

Prob(Omnibus): 0.001 Jarque-Bera (JB): 18.536

Skew: -0.911 Prob(JB): 9.44e-05

Kurtosis: 5.361 Cond. No. 1.65e+05

==============================================================================

So in the end, we find that only the C constant and the R&D Spending are really the important or most significant feature to find out if we should invest in the new business venture.

How do I believe you that by just keeping R&D feature, will improve our model accuracy?

Let’s recalculate our model using the Linear Regression library and find the difference between accuracy score

|

|

|

|

|

|

[0.8516228]

48416.297661385026

Train Score: 0.9449589778363044

Test Score: 0.9464587607787219

Let’s look at the Train score and Test Score with all the feature and with just R&D spending.

With all Features

Train Score:0.9501847627493607& Test Score:0.9347068473282446

Difference =

0.01547791542or1.548%

With just R&D spending feature

Train Score:0.9449589778363044& Test Score:0.9464587607787219

Difference = 0.0014997829424 or 0.150%

Also the if you see that the test score has improved when from 93.6% to 94.6%.

Hopefully, you enjoyed this series. In the next series, we will look at slightly more interesting topic called SVMs or Support Vector Regression.